The Capital Firewall: How to Stop Business Cash Flow From Draining Your Family's Security

Your business looks strong on paper. Your family should not be the one paying when it hits a rough patch.

You have a good month — maybe a great month — and you finally feel like you can breathe. Then a contract payment is late, a piece of equipment breaks, or a project scope changes and the invoice gets pushed back six weeks. Suddenly you are back at the kitchen table running the math again. Can you still make the mortgage? Do you skip your own paycheck this month? Do you pull from savings one more time and hope nobody notices?

If this cycle sounds familiar, you are not alone. Many veteran business owners I talk to are running profitable companies and still feel one bad month away from a household emergency. The problem is not effort. It is not revenue. It is that there is no wall between the money that runs your business and the money that protects your family.

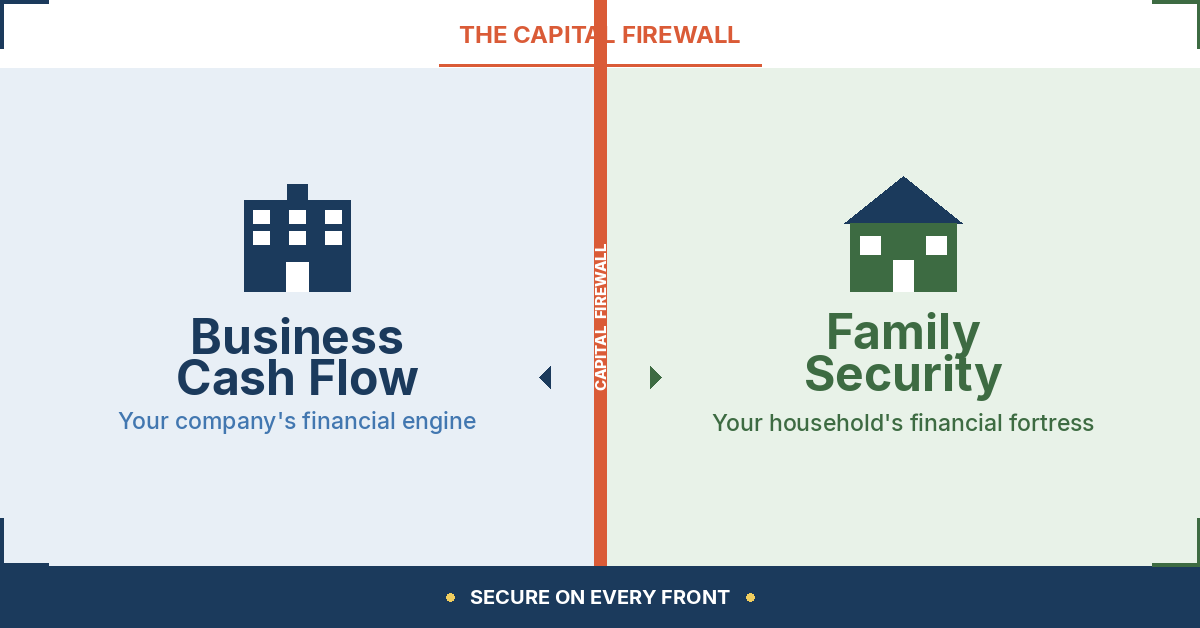

That missing wall is what I call the Capital Firewall — and building one may be the single most important step you can take to stop your family from quietly absorbing all the risk of your business.

Why Profitable Businesses Still Create Fragile Households

On paper, your business may be healthy. Revenue is up. You have clients. Your team is getting paid. But here is what often happens behind the scenes:

Your paycheck comes last. After payroll, after vendors, after that surprise expense, whatever is left goes to you. Some months that is fine. Other months it is not nearly enough. Your household budget has no floor — it just absorbs whatever the business does not need.

Savings become a business credit line. When cash gets tight, the fastest source of capital is your personal savings account, your emergency fund, or your spouse's retirement contributions. You tell yourself it is temporary. But it happens more than once, and each time the household safety net gets thinner.

Your family carries risk they did not sign up for. Your spouse sees the stress. Your kids may not understand the details, but they sense when money is tight. The business is supposed to create stability for your family — not the other way around.

This is not a business problem. It is a structural problem. And the fix is not more revenue or harder work. It is a clear boundary between business cash flow and household cash flow.

What a Capital Firewall Actually Looks Like

A Capital Firewall is not a single product or account. It is a set of decisions — built into how you pay yourself, how you hold cash reserves, and how your business and personal finances connect.

Here is what it typically includes:

A steady, documented owner-pay plan. Instead of taking whatever is left over, you set a regular paycheck that reflects what the business can sustain — not just in good months, but in average ones. This is sometimes called reasonable compensation, and it has tax and planning implications that matter. The key idea is simple: your household should not rise and fall with your business's month-to-month cash flow.

Separate reserves for business and home. Your business needs its own operating reserve — enough to cover slow months, surprise costs, and seasonal dips without reaching into personal savings. Your household needs its own emergency fund that the business cannot touch. When both sides have a buffer, one bad month does not cascade into a family crisis.

A clear line between business risk and family risk. This means your household insurance, your retirement savings, and your family emergency plan are not tangled up with your business structure. If the business has a rough quarter, your family's long-term financial security stays intact.

None of this requires a complicated strategy. It requires a plan that treats your household as its own front — one that deserves the same level of attention and protection as your business.

Why This Matters More Than You Think

When there is no firewall, every business decision becomes a family decision. Hiring someone new, taking on a larger project, investing in equipment — these are business moves, but when cash flow is tangled, your family is the one absorbing the risk if they do not go as planned.

That weight is exhausting. And it changes how you lead. You start making decisions out of fear instead of strategy. You avoid the growth moves your business needs because you cannot afford the household disruption if something goes sideways.

A Capital Firewall does not eliminate business risk. But it can keep business risk from becoming family risk. And when your family is secure — truly secure, not just hoping for a good quarter — you are free to lead your business the way it deserves to be led.

The Path Forward

If any of this sounds familiar, the first step is not a product or a pitch. It is a clear picture of where your business and household actually stand — what is protected, what is exposed, and where the line between the two needs to get stronger.

That is exactly what the Free Readiness Snapshot is designed to do. It is a short assessment that looks at your business cash flow, your household stability, and the boundary between them. No cost, no pressure, no sales call. Just a clear starting point.

From there, if it makes sense, we can sit down for a Mission Readiness Review — a one-on-one conversation where we walk through your snapshot together and talk about what a Capital Firewall could look like for your specific situation.

You built your business to give your family a better life. A Capital Firewall helps make sure it actually does.